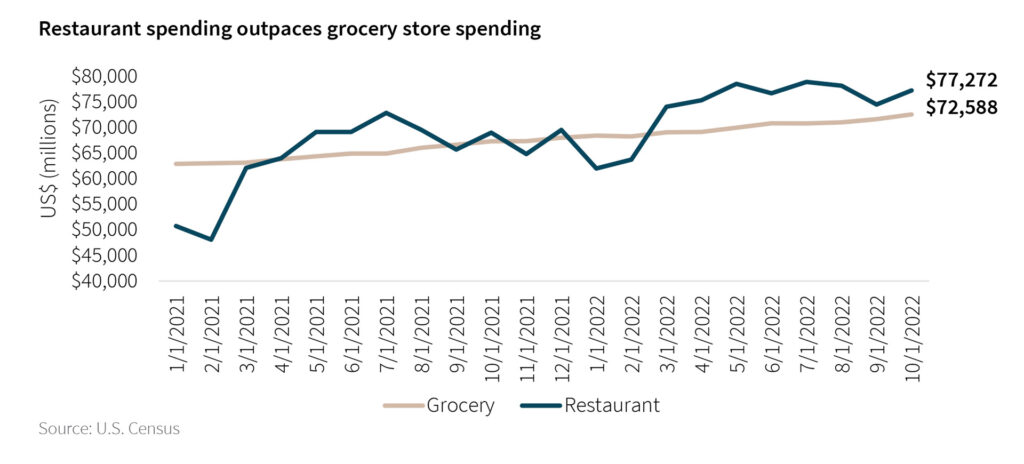

JLL released its latest Retail Grocery Outlook report, based on an analysis of trends over the previous year. After reviewing data from the Census Bureau, the report noted that, even in spite of rising prices overall due to inflation, there was still a 14.1% year-over-year increase in spending in the restaurant and bar segment. This indicates that consumers are not yet curbing their desire to dine out, and are therefore not yet spending more on grocery items for more frequent at-home meal preparations.

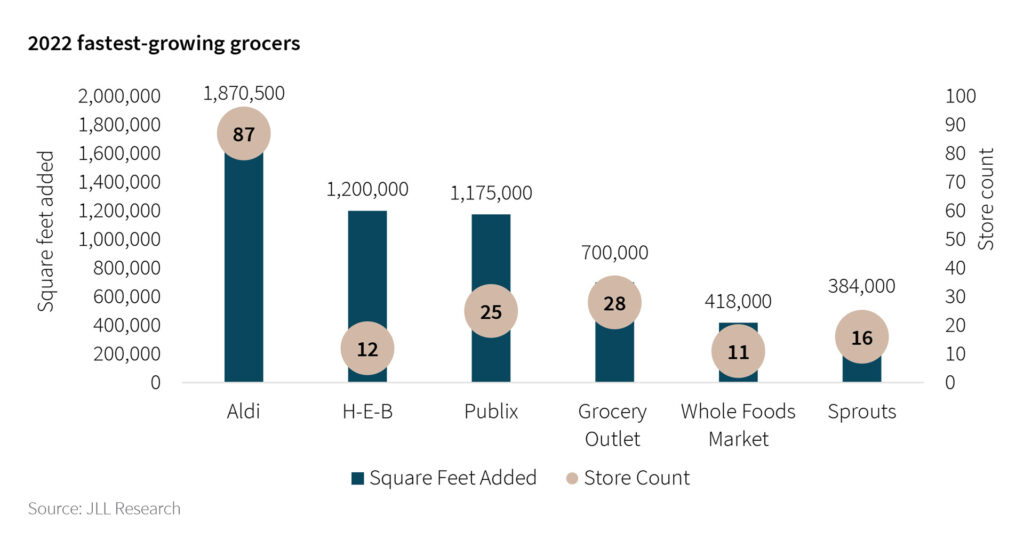

The grocery brands that had the highest number of new units open over the past year, however, happen to be the extreme value-priced grocers, such as ALDI, which opened 49 units, and Grocery Outlet, which opened 28 units. This reveals that there is a strong national demand for bargain shopping in the grocery sector. For example, ALDI is a grocer in which 90% of its merchandise is its own bargain-priced private labels, and Grocery Outlet specializes in selling both reduced price overstock items as well as its own private labels.

The report also commented on the various store size trends that grocers have experimented with this past year. With the exception of H-E-B, which is jumping on the larger store trend that many other retailers are embarking on (e.g., Target), the majority of the other grocers, such as Meijer and Schnucks, are going in the opposite direction and opening smaller sized stores. The report mentions that these small-format grocery concepts are not only cheaper to build, but because there is less land to lease, more grocery brands have access to the available space. Customers also appreciate the convenience and speed that these smaller sized grocery stores provide, as indicated by the sales of GreenWise Market – the small format version of Publix – which, according to data from Placer.ai, saw a greater year-over-year increase of customer visits compared to the Publix stores.